Zelle Limits by Bank: Daily, Weekly, and Monthly Transfer Caps

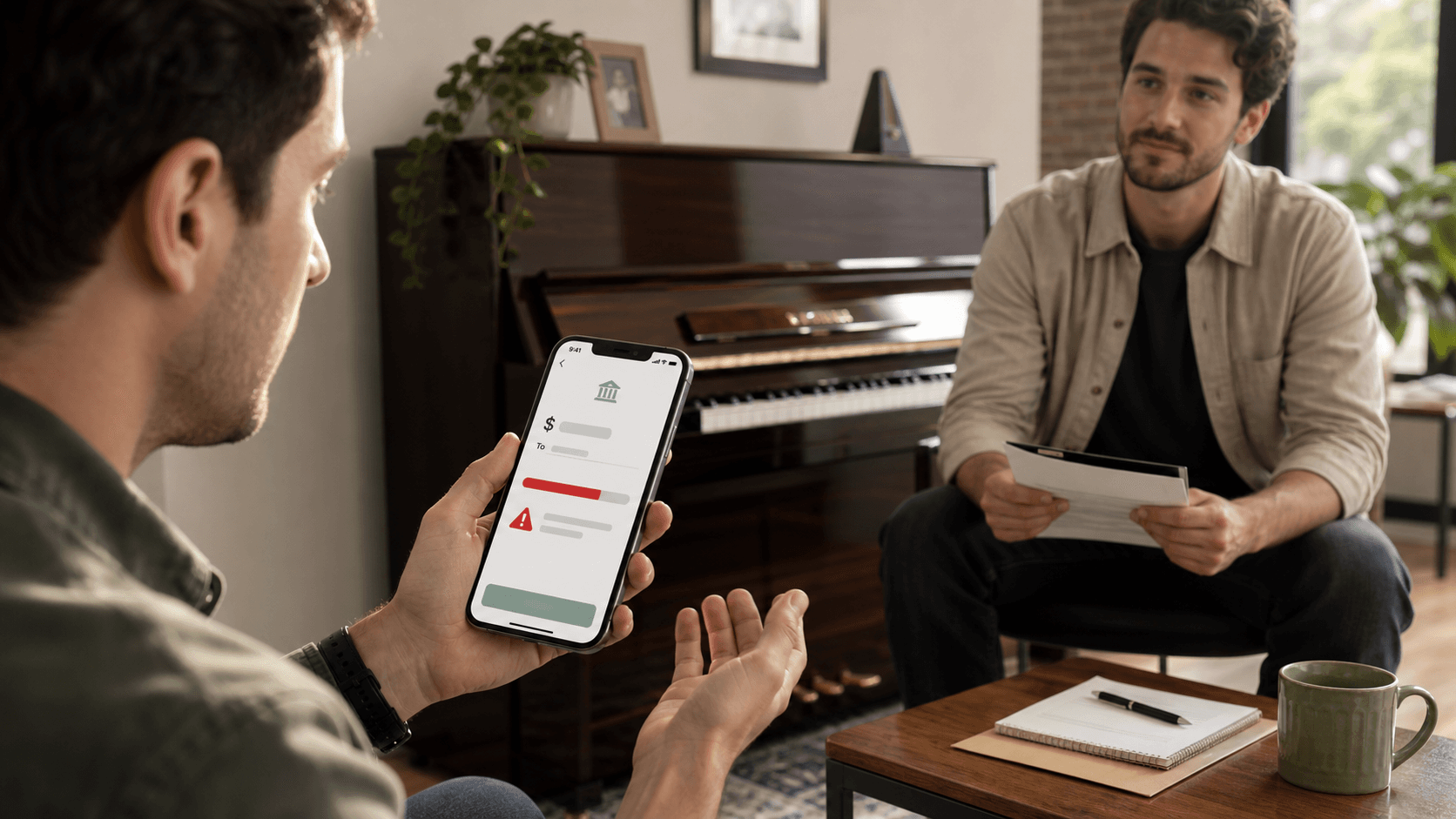

Zelle is useful when a payment is small, trusted, and inside your bank's rules. It starts to feel less simple when the payment is rent, a contractor deposit, a security deposit, a family emergency, a business invoice, or any other payment that is larger than your bank will let you send today.

That is why Check Supply built a Zelle limits directory. It maps Zelle support and researched transfer-limit guidance bank by bank, so you can check daily, weekly, monthly, and per-transfer caps before a payment gets stuck.

The short version

There is no single universal Zelle limit. Zelle's own help center tells users to contact their bank or credit union for sending and receiving limits, and banks publish different rules. Some disclose a daily cap. Some show the final cap only after you sign in. Some set lower limits for new recipients, newer Zelle enrollment, business accounts, account type, risk profile, or transaction history.

That matters because important payments rarely arrive in clean $500 chunks. If your bank lets you send $1,000 today and your rent is $3,800, you do not just have a payment problem. You have a timing problem.

Checks work differently. Check Supply payments are not constrained by Zelle-style per-transfer, daily, weekly, or monthly sending caps. If the payment needs to go out and the recipient can accept a check, just send a check.

Checks have no limits

No Zelle-style caps. Just send a check.

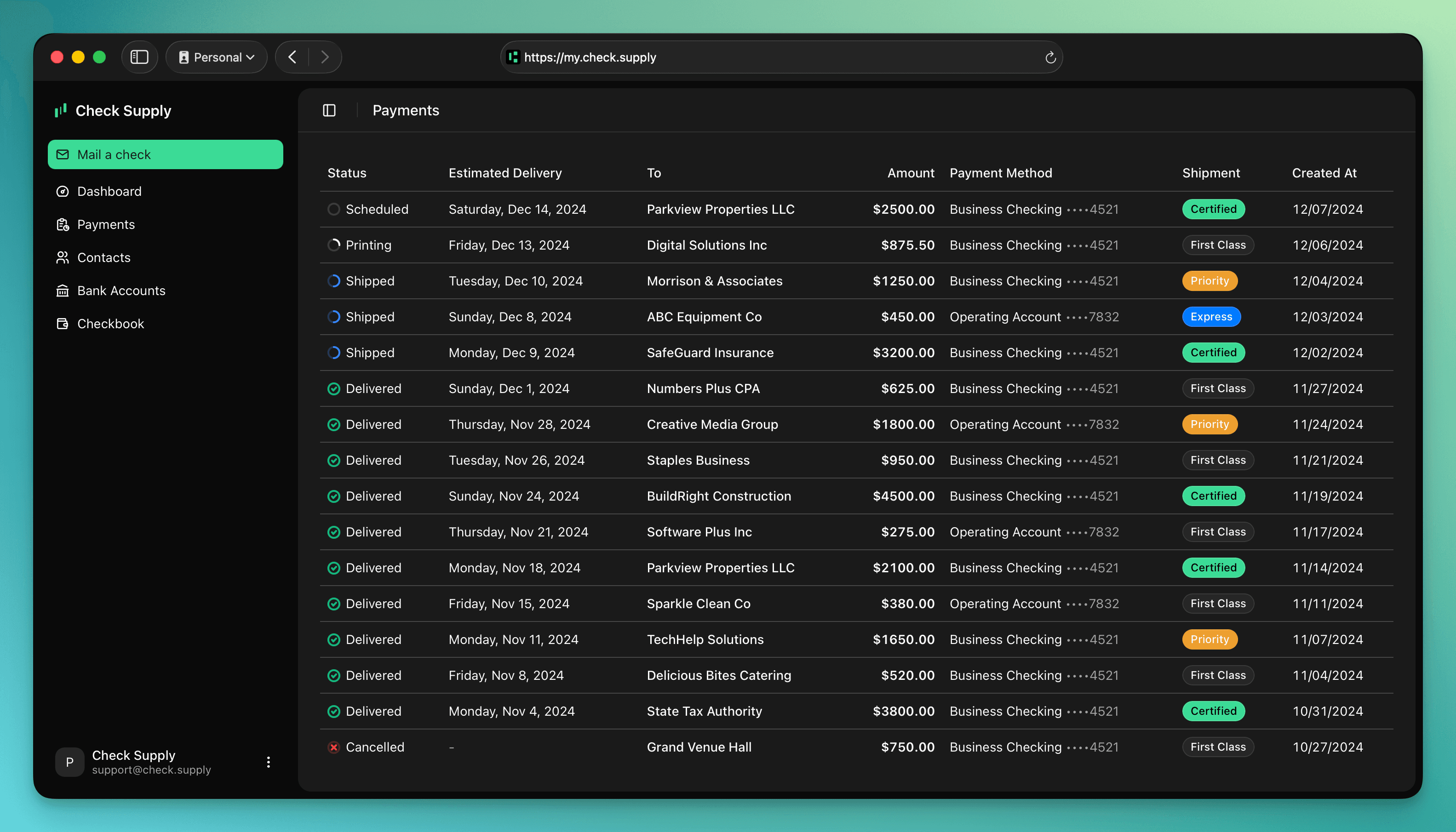

When Zelle caps the transfer, Check Supply gives you a direct check-based path for larger payments. Create the payment, choose the delivery speed, add tracking or signature-required delivery when needed, and keep a record from creation through delivery.

Why Zelle limits vary so much

Zelle is offered through participating banks and credit unions, so the transfer experience is not identical everywhere. The Zelle network moves money quickly between enrolled users, but the bank controls the sender's eligibility, transaction review, and transfer caps.

In practice, your limit can depend on:

- The bank or credit union you use

- Whether the account is consumer, small business, private client, or another relationship tier

- How long you have been enrolled with Zelle

- Whether the recipient is new, inactive, or recently added

- Whether the bank treats the payment as higher risk

- Whether your cap is measured daily, weekly, monthly, rolling, or calendar-based

- Whether you already sent money in the same limit window

That is why a payment can work one month and fail the next. It is also why two people at the same bank can see different Zelle limits.

Common Zelle use cases that can hit limits

Zelle is often used for quick personal payments: splitting a dinner bill, reimbursing a friend, paying a roommate, sending money to family, or collecting money from someone you already know and trust. Those payments usually fit the product well.

The limit problem shows up when people try to use the same rail for larger or more formal payments:

- Rent and security deposits

- Contractor deposits and home repairs

- Wedding vendors, photographers, and event venues

- Tuition, camp, or school-related payments

- Large family reimbursements or emergency support

- Facebook Marketplace purchases, especially furniture, instruments, and local pickup items

- Used cars, pianos, appliances, electronics, and other large private-party purchases

- Medical, insurance, or tax-related payments

- Small-business invoices from someone who wants direct payment

Zelle can be the fastest option when it works. But if the bank limit is lower than the amount due, you may have to split the payment across days, ask the recipient to accept another method, or move to a payment method designed for larger amounts.

Facebook Marketplace is a common place to run into this problem because the transaction is often both local and urgent. A buyer may be standing in front of a piano, couch, used car, camera kit, or appliance with the seller ready to hand it over, only to discover that the bank will not approve the full Zelle amount. That can turn a simple pickup into a negotiation about deposits, split payments, cash, or whether the seller is willing to wait.

For large purchases and private-party transactions, plan the payment method before you meet. Check the bank's Zelle cap, confirm whether the seller accepts checks, and avoid assuming that a mobile transfer can cover the full purchase price just because the account has enough money.

What official sources say about Zelle limits

The important research finding is not just that banks have limits. It is that they describe those limits differently.

Source | What it shows |

|---|---|

Zelle FAQ | Zelle directs users to their own bank or credit union for sending and receiving limits. |

Chase | Chase says it applies a daily send limit even if your available balance is higher, and dynamically determines the transaction tier when you set up the payment. |

Bank of America | Bank of America publishes daily, weekly, and monthly Zelle limits, with lower limits during the first 60 days of initial enrollment. |

Wells Fargo | Wells Fargo publishes rolling 24-hour and rolling 30-day limits, with higher published limits for eligible small-business relationships. |

PNC | PNC tells customers to view daily and calendar-monthly send limits inside the PNC Mobile app. |

Capital One | Capital One's terms say transfer amount and frequency limits can be flexible, risk-based, and modified without advance notice. |

That is the behavior the Check Supply Zelle limits directory is built to surface: not just whether a bank supports Zelle, but what kind of cap a sender should expect before they rely on it.

Why planning around Zelle limits matters

Large payments often have deadlines. Rent is due on a certain day. A contractor may need a deposit before they order materials. A private seller may not hold an item while you wait for tomorrow's transfer window. A family member may need funds today.

If you do not check your Zelle cap first, you can run into problems at the worst possible time:

- The bank rejects the amount when you enter it

- The app shows a lower remaining limit because of payments you already sent

- The recipient is new, so the bank applies a smaller cap

- The bank's limit is rolling, so it does not reset at midnight

- A weekly or monthly cap blocks the second half of a split payment

- The recipient does not want to receive multiple partial payments

The fix is simple: look up the bank first, then decide whether Zelle is actually the right payment method.

How to use the Check Supply Zelle limits directory

Start at /zelle. Search for your bank, open the bank page, and review the published or researched limit guidance.

The directory includes more than 1,400 Zelle-supported institutions from Check Supply's mapped dataset. For each institution, we show support status, enrollment context, available source links, and limit research when it is published or can be reasonably verified.

Use it as a planning tool:

- Search your bank before promising a Zelle payment.

- Compare the amount due against the bank's daily, weekly, monthly, or per-transfer cap.

- Confirm the final limit inside your own banking app before sending.

- If the payment is larger than the cap, send a check with Check Supply instead.

When a check is the better answer

A check is better when the payment has to be larger than your bank's Zelle cap, when the recipient needs a familiar payment instrument, or when you want a delivery record instead of a transfer attempt hidden inside a banking app.

Use Check Supply when:

- The payment exceeds the Zelle limit shown by your bank

- You do not want to split one obligation into multiple partial transfers

- The recipient does not use Zelle

- The recipient wants a check for bookkeeping, rent records, vendor records, or internal approval

- You want mail tracking or signature-required delivery

- The payment is important enough that guessing the bank's limit is not acceptable

Checks have no Zelle-style caps. There is no Zelle daily limit, weekly limit, monthly limit, or per-transfer cap on a mailed check through Check Supply. Ordinary banking rules still apply, including having funds available and sending a valid payment, but you are not working around Zelle's limit system.

Frequently asked questions

What is my Zelle limit?

Your Zelle limit depends on your bank or credit union. Search the Check Supply Zelle limits directory, then confirm the final amount inside your bank's app before sending.

Is there a universal Zelle daily limit?

No. Zelle does not publish one universal daily limit for every user. Banks and credit unions set their own rules, and many adjust limits by account type, recipient, tenure, risk controls, and transaction history.

Can I avoid a Zelle limit by splitting the payment?

Sometimes a split payment works, but it is not reliable. Banks can apply aggregate daily, weekly, or monthly limits, and the recipient may not want multiple partial payments. For important payments, check the limit first and use a check if the amount is too large.

Do checks have Zelle limits?

No. Checks are not Zelle transfers. A Check Supply mailed check is not subject to Zelle per-transfer, daily, weekly, or monthly caps.

Where should I start?

Start with the Zelle limits directory. If your bank's limit is too low, send the payment as a check instead.